Meeting your clients’ expectations | Making Digital Easy | Part 1 of 7

In this series, we will show you how to use digital technology within your business to transform your everyday processes, enhancing client loyalty, increasing profitability and delivering compliance confidence.

The seven-part series will cover the following topics -

-

Meeting your clients’ expectations.

-

Using digital to transform your everyday business processes.

-

Going from Good to Great

- Using your app with your next generation of clients

- What’s my back office for?

- AI and the future of financial services

- Keep it simple and on-brand

Like this article? There's more where that came from. This is part of a 7-part series on Making Digital Easy. To view the full guide, click below.

Digital transformation

Wikipedia defines Digital Transformation as “The adoption of digital technology to create new or modify existing products, services and operations by translating business processes into a digital format. The goal is to increase value through innovation, invention, improved customer experience and efficiency.”

There are lots of examples in our everyday life such as online banking, shopping, parking, booking a cab, listening to the radio, and watching TV,. all of which have been transformed by digital technology. Digital transformation is an evolving process as technology becomes ever more capable. There are three stages to digital transformation, starting with the internet which changed how we use and think about technology -

Stage one – the internet

We have got used to using Google, online banking, online shopping etc. and this was really accelerated during Covid when video conferencing became a critical engagement tool and forced every one of us, who wanted to communicate with anyone, to use a PC or tablet.

Stage two – the smartphone

The smartphone brought the ability to access the services we use, wherever and whenever we need. Let’s face it, everyone’s delivering you an app on your phone. I even have one now to check my local council bin pick-ups. Did I think I needed this as an app? No, but it’s a lot easier than having to go to my PC and login to a website to find out what bins are being picked up this week.

Given the proliferation of apps that your clients are using it’s easy to understand why your clients’ minimum expectations are that they can access your services through an app on their phone.

Stage three– Artificial Intelligence (AI)

AI will really shake things up and we’ll explore how AI can already have a positive impact on your services in a later article.

We’re currently somewhere between the middle of stage 2 and at the very beginning of stage 3. It’s an exciting time to be in digital technology as AI will change our lives to an even greater extent than the internet and smartphones.

Are you ready to take your client engagement to the next level?

For more information and to organise a personal demonstration please click below.

An example of digital transformation - the humble parking app

The parking app is now integral to pretty much every car park and town centre. The apps were initially clunky – often requiring a password and different parking apps were required to pay for parking at different carparks. The number of different apps is falling significantly and most use biometric security which is so much easier than trying to type in a password on a mobile phone. If you are parking around my town, Leamington Spa, most of the machines no longer take cash. As the machines break they’re not fixed. The council rely on RingGo and, if you want to park, you have to use the app.

If like me you pop into town most days to pick up shopping, walk the dog etc. the app is so much easier than carrying around change for the parking meter. It takes a few seconds to pay for parking and the app reminds me if my time is running low. It’s a better way of paying for parking for the end-user as there’s no change to carry. As long as I’ve got my smartphone I can pay for parking.

But now consider how it’s also better for the council – no cash to collect, machines to fix and they can increase prices with little or no work. Increasing prices may be not so good for me but ultimately, we all save as the council raise more money with less cost and can hopefully spend the money on better things than fixing parking meters. Potholes spring to mind, particularly if you live in Daventry.

See Daventry Banksie for an amusing read.

The key thing here is that parking has changed because adoption of the app(s) has been achieved. Partly through making the service better for the end user and partly because you have no choice. My eighty-seven year old Mum was annoyed she can no longer park without using the app. Her grandchildren showed her how easy it was to use and now even she’s a convert. Not through choice, but necessity is the mother of invention as the saying goes.

Financial advisers and wealth managers have had limited success in implementing client portal technology particularly through their platforms or back-office systems and that’s because you can’t get the benefits of digital transformation unless you think about the problem from your client's perspective.

Your new role as your client’s technology supplier

You need to consider that you are extending your role from that of adviser to a technology supplier, as it’s your technology that you want your clients to use. As a technology supplier, it’s important that you think about the experience from your client’s perspective. This is the key to success. You need to deliver a technology solution that meet’s your clients’ expectations. If you don’t then all the benefits of a digital servicing channel will be lost to you. However, meeting your clients’ expectations is not as hard as you think.

Meeting your clients’ expectations

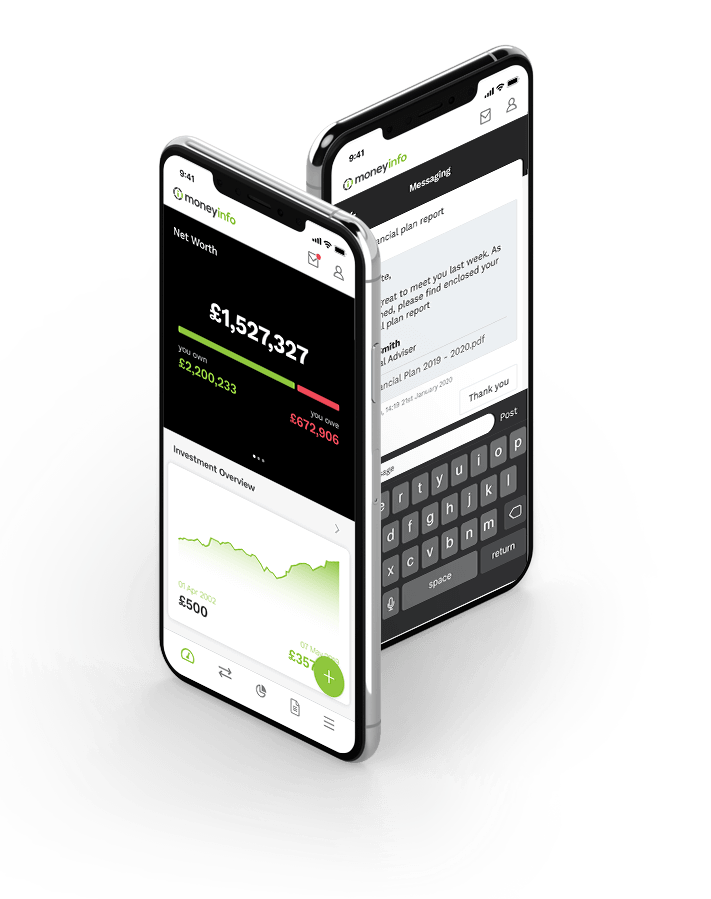

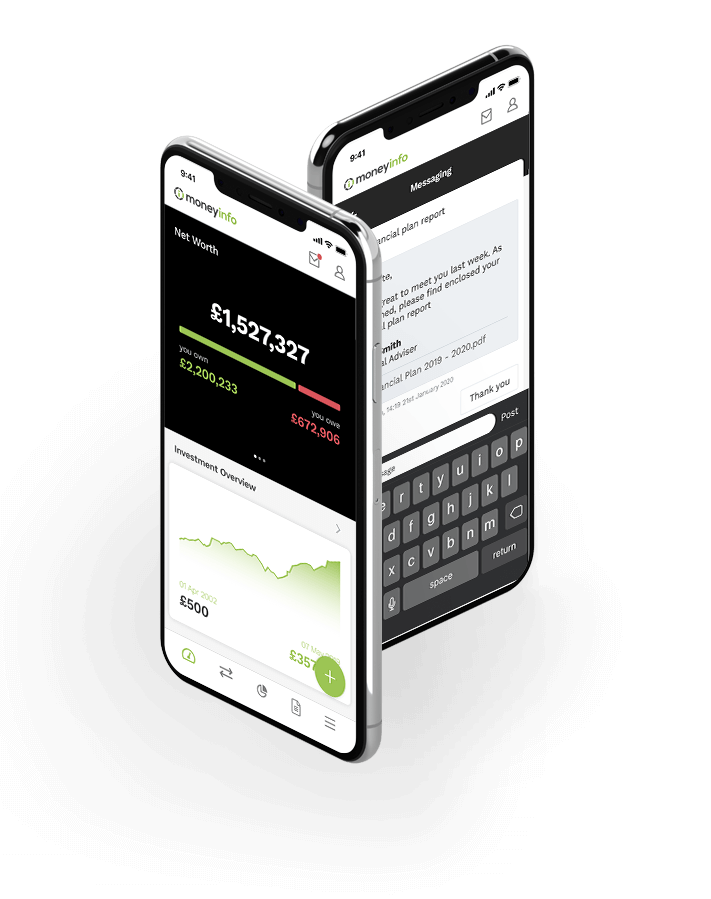

Your clients expect to access your services through whichever technology they have to hand when they receive a note from you. That means it’s got to be an app and one that makes their lives easier and is an obvious improvement on the old way of doing things. Your clients will use your app if –

- You deliver them an app to access your services, conveniently across all the technologies they use – their laptops, tablets and smartphones.

- It uses biometric security so they don’t need to type a password and deal with multi-factor authentication to access their data or read a letter from you.

- They can view their investments and their data is regularly updated.

- Communicating with you is secure and as easy as talking with their friends via WhatsApp, with video, pictures and even emojis as part of the compliance record.

- They can keep track of and access all their important financial paperwork whenever and wherever it suits them.

-

When they want to see you, they can book an appointment.

Adoption is key to your success, so it needs to be managed and it’s unlikely to be achieved on day-one as the natural habit is for both your clients and your staff to fall back into using email as it’s not easy to break a habit. But you’re doing this for a good reason and it’s going to benefit your clients because –

- They want to check their wealth. Not because they want to trade. It’s just reassuring to know they can view it whenever they want and see how it’s performing.

- They are uncomfortable with sending their financial information over email and they’re very uncomfortable with clicking on email links that ask them to sign paperwork. Worse still, some of your really important emails get lost in their junk folder which is not a great reflection on your service.

-

The paperwork you deliver them is important. They want it. They value it. They know it’s important. They just don’t know where to store it so they can access it when they need it.

Three things

Clients generally want three things from your app - access to their valuations, a secure way to communicate with you and their paperwork organised. If you deliver these so they can access them conveniently and easily then you’re on your way to complementing your adviser services with a digital service channel.

At times, existing clients will revert to using email. When they do, bring the email into your digital service and respond via secure messaging. Your client’s will get a push notification on their phone, allowing them to access the response with a simple biometric login, reassuring them every time they login that you’re taking their data protection seriously. Pretty soon, they’ll use the app as it’s more convenient and easier to communicate with you than email, it’s easier than the old way of working – i.e. they don’t need to think about who they are communicating with, the information can be tracked for them, it’s secure and they know they are safe from phishing attempts. An easier and better way for them to interact with you.

For new clients, adoption is easier. If you give them access to your client portal from the outset, your onboarding journey can be delivered through your app. Your client learns to communicate with you through your app. They will love seeing their fact find take shape and having all their paperwork organised – and let’s face it – there is a lot of paperwork.

Remember, if it’s a better way of working for your clients and you are consistent in using it, eventually you’ll reach critical mass and then like the council you’ll need to decide if you let the odd client continue to use post and email. That’s your decision based on the value to your business of a single way of working vs. the cost of dealing with the odd exception.

This is the beginning of your digital journey but it's sadly the end for many client portals. If you don’t look at the technology from your client's perspective then you won’t get to enjoy the great efficiencies that digital servicing can provide. We’ll explore these in the next article.