UK Watchdog makes it easier to deliver account aggregation to your clients

Check out the various news reports below to see how the landscape is changing for consumers (some of whom are your clients) to manage their overall finances in one app:

Your clients will only ever need one of these apps. Here’s what you need to consider and why you are in a prime position to offer this now, before the banks do.

The Competition and Markets Authority (CMA) has concluded after a two year probe that consumers will be better off accessing details of their entire finances through a single app (no sh!t Sherlock!).

The primary driver is to increase competition and better identifying account charges on everyday banking and credit card accounts. Banks have been told that they must make it easier to access their information in one place even if they are currently managed by different providers. This is strengthened by rules passed by the European Parliament in 2015 where banks must sign up for open banking, or Application Programme Interface (API) standards which makes it easier for other companies to connect to them and retrieve customer data. This will ultimately lead to the UK banks themselves (as they have in the US) offering account aggregation to their customers in order to maintain the primary relationship. The race is on for your business to get there first. If you own the interface, you own the client relationship.

It is accepted one of the biggest hurdles to the adoption of account aggregation is cultural. UK consumers on the whole would not currently trust a provider with so much sensitive information like their spending habits and transactions. However culture and trust changes over time once technology becomes more acceptable. How many consumers did not trust online banking when it was first introduced? How many people thought the idea of sharing and storing their personal photo albums and interests on the web thought it was a bad idea?

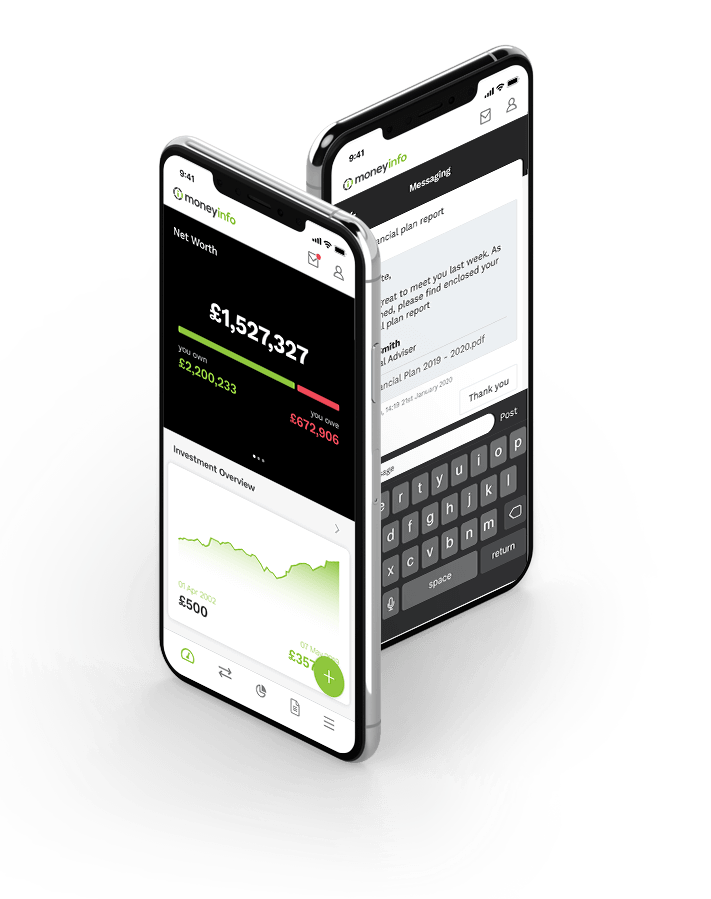

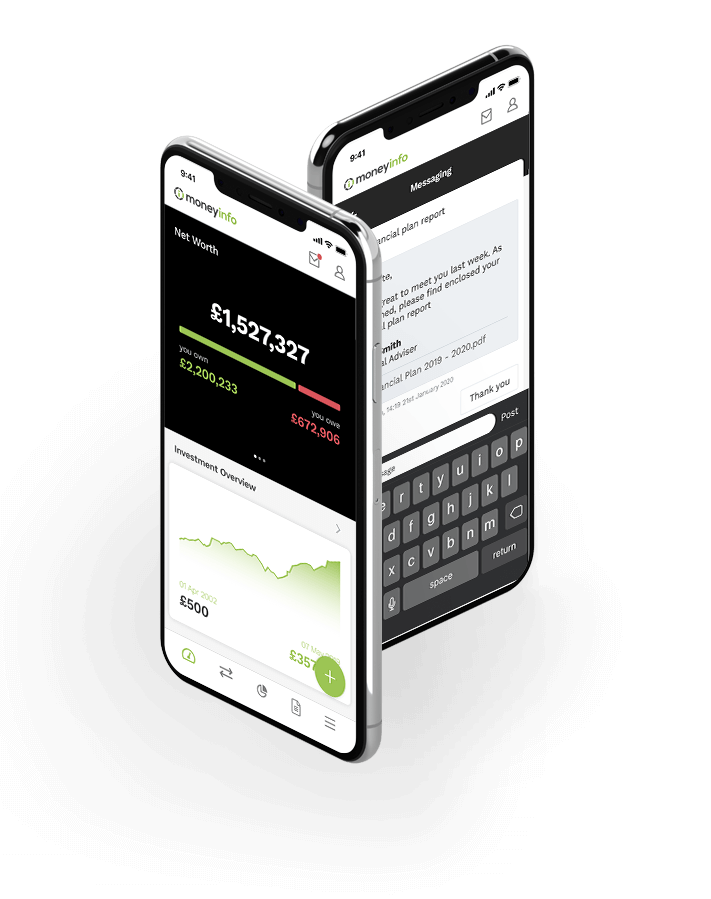

An app that can aggregate your entire financial life exists today in a number of forms and your clients will only ever need one of these things. You do not need to deliver all the bells and whistles from day one as adoption inevitably takes time. Start with delivering what you currently do for them (portfolio management and documentation) so they get used to interacting with you digitally. Introduce enhanced account aggregation over time and let them find their own comfort levels with it accompanied by regular communications extolling the benefits, convenience and security of aggregating their finances

So it’s worth seeking out what can work with your business so you can control the financial interface for your clients sooner than later.

Financial advisers, wealth managers and workplace consultancies can have a supercharged head start in owning the aggregated financial interface for their clients for a number of reasons:

- Advisers have closer relationships with clients than the banks do.

- Advice firms have the golden ‘agency code’ with third party providers that already authorises them to gain information on the client’s behalf and create a holistic picture of their ‘entire’ wealth. The right app will make that über efficient. Why wait for the industry to sort their act out and have a level playing field? Capitalise on your vantage point.

- Aggregating personal finances, properties, other assets and documents for purely holistic reporting creates more trust because you are not trying to ‘mine’ their data and flog them something else.

- Advisers have a reason to introduce this technology to clients to streamline their interactions. If all of a consumer’s accounts are in one place, so is their income and expenditure which is fundamental for the suitability of ongoing advice. It is closely related to what you already do.

- Advice firms can help with other aspects of their finances like organising the ‘bag for life’ financial filing cabinet and returning it to clients as a service in its own right. People pay for convenience.

- Advice firms can demonstrate use of big data genuinely in the interests of the client. For example, if they are under insured, off track for a specific goal or reaching their lifetime allowance limit. Aggregated data can be used for proactive advice rather than waiting for an annual review (which many people do not value paying for).

Register for our next moneyinfo webinar and we will show you how to create an aggregated financial interface for your clients.