Using your app with your next generation of clients | Making Digital Easy | Part 4 of 7

In this series, we will show you how to use digital technology within your business to transform your everyday processes, enhancing client loyalty, increasing profitability and delivering compliance confidence.

The seven-part series will cover the following topics -

- Meeting your clients’ expectations.

-

Using digital to transform your everyday business processes.

-

Going from Good to Great

- Using your app with your next generation of clients

- What’s my back office for?

- AI and the future of financial services

- Keep it simple and on-brand

Like this article? There's more where that came from. This is part of a 7-part series on Making Digital Easy. To view the full guide, click below.

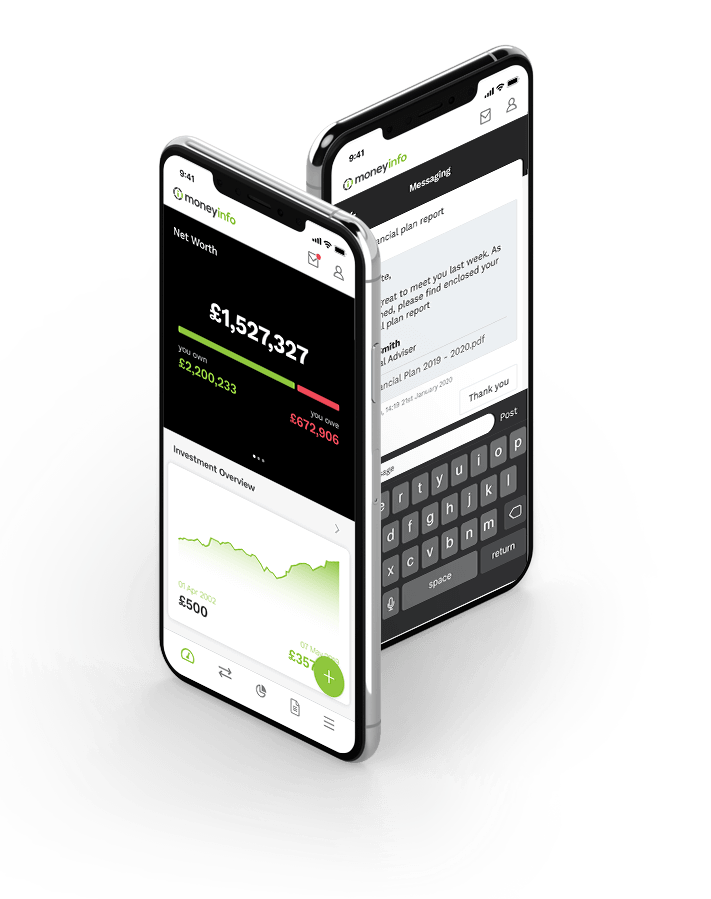

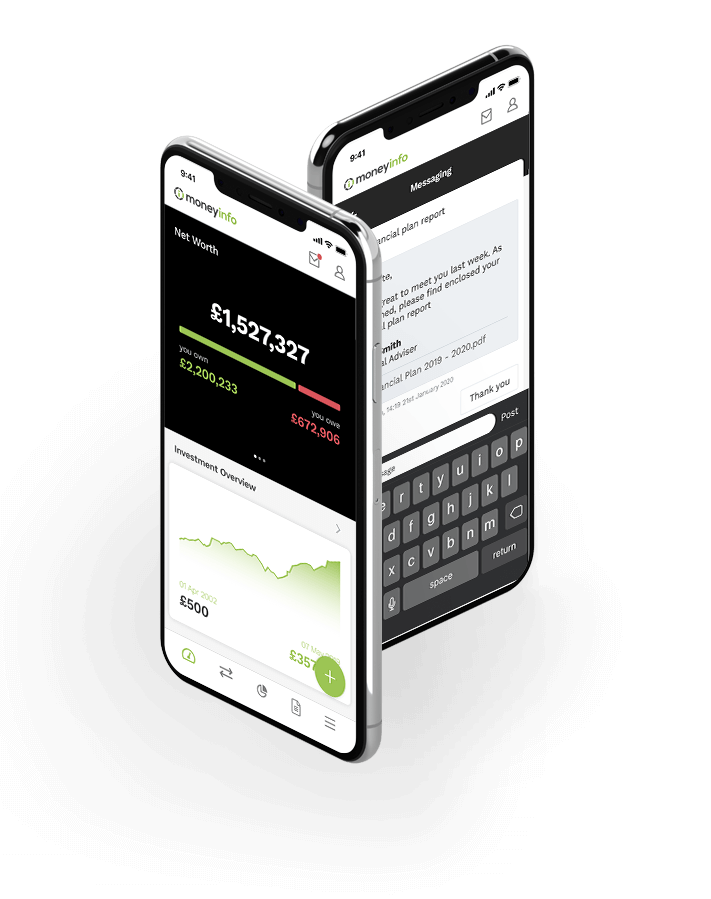

In part one, we looked at the three things that will get clients using your app. These were access to their valuations, securing their communications and organising their paperwork. Before we look at how you can use your app to attract the next generation of your clients, it’s worth exploring how your app can become your client’s go-to financial app, in case of emergency.

A word about data.

First a word about data as this is often a sticking point for firms wanting to go digital. If you’re going to give your clients access to their valuations, it’s important that your data is clean and regularly updated. It might be okay to update your back-office data to support your client reviews and regular reporting once or twice a year but if you’re putting your data online so your client can view it at any time, then it’s important it’s up to date.

To make this easy for you, we manage the data on your behalf working with your providers and platforms to ensure that the data feeds are successful and handling any errors on your behalf.

Wherever possible, the data is updated daily on an overnight scheduled basis, ensuring that when your client opens their app, they get access to the latest data immediately. One of the benefits of the portal that you’ll quickly come to appreciate is that you have access to up to date valuation information too, through the moneyinfo manager app. Having up to date data means your management information is accurate. You can confidently know how your AUM is growing,

helping you monitor the value of your business.

Having a portal not only helps you to grow the value of your business, it adds value to your business too. Businesses with digital client engagement are more efficient and worth more than those without. Advice firms are ‘more valuable’ with a client portal.

Clients like being able to see the value of their investments, even though this is counter-intuitive to your advice which asks them to think long-term and not worry about short-term market movements. But the truth is, we like to view our wealth as it’s reassuring to know that it’s there and it’s backing up your service which is delivering financial peace of mind.

Clients like being able to see the value of their investments, even though this is counter-intuitive to your advice which asks them to think long-term and not worry about short-term market movements. But the truth is, we like to view our wealth as it’s reassuring to know that it’s there and it’s backing up your service which is delivering financial peace of mind.

In case of emergency

To go further and for your app to become your client’s go-to financial app, you need to consider what’s helpful to your client over and above the service you deliver. For instance, you manage the client’s investment portfolio but is that everything they consider to be a financial asset. Most clients would consider their property, cars, boats, art collection and for some, their wine collection as part of their wealth. More importantly, all this stuff comes with pain (except the wine collection which is a disappearing asset !-). The pain is they need to insure it and this is where the secure storage of paperwork in your portal is really helpful for your clients.

Your clients are likely to have more than average complexity in their financial lives. They may have more than one property, a holiday home or buy-to-let investment, and a number of cars particularly if they have older children. All of this stuff needs to be insured and produces significant amounts of paperwork. Your client needs to store this in a convenient place so they can access it in an emergency. If they have property abroad, a filing cabinet doesn’t really help but having access to all their paperwork through your app, really does. As the one thing that’s with them all the time is their smartphone.

Are you ready to take your client engagement to the next level?

For more information and to organise a personal demonstration please click below.

Clients will find that adding a copy of their passports when travelling, along with their travel insurance information will be really handy in an emergency. Keeping details with the asset such as your home insurance with your property, car insurances with the cars makes finding things in an emergency easy. Your client only needs one incident where they rely on your app to retrieve information and they won’t want you to take away their app from them. Your app is adding to their financial peace of mind, complementing the service you deliver.

Add to this the reassurance of a folder containing their will and other important documents such as life assurance etc.

They can let their next of kin know that in case of emergency they just need to contact you, their financial adviser and you’ve got access to all the important paperwork. This puts you in the driving seat if the worst happens and you need to begin a relationship in difficult circumstances with your next generation of clients.

Your clients are getting older…

It’s pretty obvious but every year your clients are getting older, and this is a risk to your business growth. As an example, in 2022 the Abrdn platform had 430,000 customers and their average age was 63.

A lot has been written about the intergenerational wealth transfer, with some £5.5trillion expected to be transferred over the next 30 years...

And £337bn potential HNW inheritances over the next ten years to 300,000 younger potential clients according to FT Adviser.

Back in 2021, Schroders published a practical guide to intergenerational wealth transfer which highlights some steps to identifying the size of the problem facing advisers.

Auditing your business - do I have a problem?

- Identify clients by age groups, for example 60s, 70s and 80s.

- Identify the assets under management in each group.

- Identify the fee income generated from each.

- Assume that 65% of this income leaves your business over the next few years.

The table below is an example of this approach and whilst just a simple illustration, it potentially gives an indication of the impact on your business.

Schroders go onto provide a more detailed approach to reviewing a client segment, for example, looking at those in their 70s or 80s -

- List their family names, marital status, assets under management, actual fee income and dependents.

- Assess your level of engagement with those family members using a simple ‘high’, ‘medium’ or ‘low’ categorisation.

- Assume that those family members with ‘low’ and ‘medium’ engagement move to a different adviser, this will enable you to identify the potential impact on your business.

It’s important to consider that the next generation of your clients will be different.

The oldest millennials will be 43 in 2024. Millennials make up almost one-third of the global population and account for around half of the global workforce. Together with their successors (known as Generation Z),

they will account for almost three-quarters of the workforce by 2030.

Millennials grew up with the internet and are “digital natives”. They are enthusiastic adopters of new and innovative technologies that fit in with their lifestyle choices. They like smart technology for phones, tablets, cameras, speakers, TVs, and credit cards. Wi-Fi is their oxygen, and they live and breathe online through social media and the cloud.

And then Gen Z, those born between 1997 and 2012, were practically born with phones in their hands, meaning they are constantly connected and hyperaware of global goings-on. With that comes great concern for their personal image, strong opinions and high expectations.

“Two-thirds of inheritors will fire their parent’s adviser when they inherit.”

According to the Schroders research, 65% of inheritors do not intend to continue using their parents’ financial adviser after they receive an inheritance. Wealth transfer is a growing threat to adviser firms but for adviser firms who get their act together it is also a great opportunity. Many of these new inheritors will not have enough assets for the private banks and wealth management firms that have looked after their parents.

Social Media for Good or Bad…

Through their social media networks, the children of your clients could be your best advocates in attracting these new inheritors as they will naturally share a job well done with their friends. For good or bad, depending on your relationship, their network will connect you to these new inheritors. With that in mind, what can you do now to ensure the children of your clients not only remain your clients when the wealth passes to them but become advocates for you in the hunt for new assets.

It’s going to be expensive to offer face to face advice to the next generation and they may not need it right now, but creative use of digital technology can help you to cost effectively build a relationship.

The technology you provide your clients’ children should help them manage their finances, though of course for them to use it, it must be available as an app for their smartphone. Your future clients will appreciate being able to monitor their savings, pensions, investments, personal finances, property, insurances and debt together in one place and will also benefit from any relevant news that helps promote good savings habits.

Be there to help them in the moments that matter.

They will love having one easy place to store all their financial paperwork knowing it is secure and accessible when they need it. Your app can provide them with a secure way to communicate with you so that if they have any questions or concerns you can be a first port of call. You will be there to help them in the moments that matter.

Reinforcing your existing relationship.

By using technology with the next generation, you are reinforcing your relationship with your current clients. Subject to agreement to share data, you can provide views across the whole family bringing together client, partner, trusts, dependents, and business accounts. And for estate planning, the net worth statements will combine to provide a family balance sheet to identify potential IHT liability and help you to propose solutions to reduce the liability.

You can work with your current clients to create an ‘In Case of Emergency’ (ICE) folder in which to store everything of relevance including copies of wills, trust deeds and lasting powers of attorney together with all the relevant paperwork for insurances, property deeds etc. This means that should the worst happen, you can provide the family with all the information and paperwork to calculate the estate, supporting the executor and speeding-up the process of probate.